Mobility and flexibility are key qualities for gaining a foothold and succeeding in the labour market. This often involves relocating, which is why we would like to draw your attention to the tax deductibility of moving expenses.

Change of Residence for Professional Reasons

If you change your place of residence for professional reasons, the resulting expenses may, under certain conditions, be deducted as income-related expenses (Werbungskosten).

A professional reason is assumed in the following cases:

Change of workplace

e.g.:

- Moving to another city when starting a career

- Relocation to another city associated with the relocation of the employer, for example when the company's registered office is moved

- Change of employer and the related moving expenses to another city

Shortened commute

The tax authorities readily recognise a professional reason if the move results in a total time saving of at least one hour for the round trip between residence and primary place of work. In this case, it is not necessary to change your place of residence. This is therefore particularly relevant for moves within large cities that result in a substantial time saving.

Which Costs Are Deductible?

A fundamental requirement for deducting income-related expenses: invoices and receipts must be retained as proof of the costs incurred. In some cases, flat-rate income-related expenses may also be taken into account:

- A flat rate of 30 cents per kilometre driven for trips between the old and new residence (also, for example, for apartment viewings)

- Broker commissions for arranging a rental property

- Double rent payments for up to six months, for example because you had to observe the notice periods of your previous apartment

- A maximum of three months' rent for your new apartment, for example because it cannot yet be used

- Transport costs for household goods

Furnishings that you purchase for the new apartment, however, are considered private living expenses and are therefore not tax-deductible.

For your other moving expenses, instead of the actual expenses, you may additionally deduct a flat-rate amount for income-related expenses, the so-called moving expense flat rates. Other moving expenses include in particular:

- Re-registration costs for the car, telephone connection and place of residence

- Cosmetic repairs in the old apartment

- The installation of a kitchen or other electrical appliances / fitting of lamps and curtains.

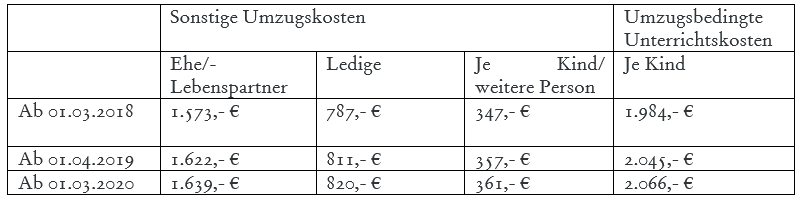

For moves in the years 2018 – 2020, the following moving expense flat rates apply pursuant to the BMF letter of 21 September 2018 (Az. IV C 5-S 2353/16/10005), for example:

If you have already moved again within five years, you may benefit from higher flat rates. In these cases, the flat rate for other moving expenses increases by 50 percent.

If your children are struggling at their new place of residence due to a change of school and therefore require tutoring, you can also claim move-related tuition costs.

Tip: If you change your place of residence because of a new job, you should ask during contract negotiations with your new employer whether they will cover the moving expenses. As an alternative to deducting income-related expenses in your tax return, the employer can reimburse the entire tax-deductible costs free of wage tax and social security contributions, provided that the move is in the particular interest of the company.

Change of Residence for Private Reasons

Not only a new job, but also new family members or simply the desire for a change: there are many reasons for relocating.

Even if you are moving for purely private reasons, you can claim part of the expenses as part of the tax reductions for household-related services pursuant to § 35a EStG. For example, if you have hired a moving company or have renovation work carried out at your apartment by a tradesperson. In principle, only labour costs and travel costs are tax-privileged; the tax reduction cannot be claimed for material costs.

Under this tax reduction, expenses of up to 20,000 euros per year can be claimed. You then receive 20 percent of the deductible expenses, but no more than 4,000 euros, as a tax reduction.

Frequently asked questions

Frequently asked questions

When is a relocation considered job-related?

A job-related reason exists if the move is connected to a change of workplace, for example when starting a career, relocating the company headquarters, or changing employers. A job-related reason is also recognized if the daily commuting time between home and the primary place of work is reduced by at least one hour. In this case, a change of city is not required, so moves within the same city may also qualify.

Which moving expenses are deductible as work-related expenses?

Deductible items include in particular transport costs for household goods, broker fees for a rental apartment, travel costs (30 cents per kilometer, e.g. for apartment viewings), duplicate rent payments for up to six months, and up to three months' rent for the new apartment that is not yet usable. Receipts must be retained. Not deductible, however, are purchases for new furnishings, as these are considered private living expenses.

What does the relocation lump sum for other moving expenses cover?

Instead of providing individual receipts, other moving expenses can be claimed via a lump sum. This includes, for example, re-registration costs for car, telephone and residence, cosmetic repairs in the previous home, and the installation of kitchens, appliances, lamps or curtains. The amount of the lump sum is determined by the BMF letter dated 21.09.2018. In the event of another move within five years, the lump sum is increased by 50 percent.

Are moving expenses also tax-deductible for private relocations?

For purely private relocations, no deduction as work-related expenses is possible; however, household-related services under § 35a EStG can be claimed. Eligible costs include labour and travel expenses of, for example, a moving company or tradesperson, but not material costs. The tax reduction amounts to 20 percent of the expenses, capped at EUR 4,000 per year on a maximum of EUR 20,000 in eligible expenses.

Can the employer reimburse relocation expenses tax-free?

Yes. If the move is in the employer's particular business interest, the employer may reimburse tax-deductible relocation expenses free of wage tax and social security contributions. Such reimbursement is an alternative to claiming the costs as work-related expenses in your own tax return. We recommend raising this point during contract negotiations with the new employer.