© C-PROMO.de

People with disabilities have the option of applying for a disability lump-sum allowance (Behinderten-Pauschbetrag) to cover their daily disability-related living expenses. Individual proof of expenses is then not required.

On 29 July 2020, the Federal Cabinet adopted the draft of a law to increase the disability lump-sum allowances and to adjust further tax provisions.

To adjust the disability lump-sum allowances and simplify the tax rules, the following measures are specifically planned:

Doubling of the disability lump-sum allowances

The disability lump-sum allowances under § 33b Abs. 3 EStG are to be doubled.

For persons with disabilities who are helpless within the meaning of § 33b Abs. 6 EStG, and for blind persons, the lump-sum allowance is to be increased to EUR 7,400 (previously EUR 3,700).

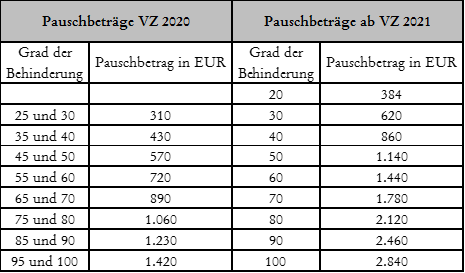

Update of the system

At the same time, the outdated system regarding the degree of disability is to be aligned with social law. In future, a disability should already be determined from a degree of disability of 20 (previously 25), with the system continued in steps of 10 up to a degree of disability of 100:

Introduction of a disability-related travel-cost lump-sum allowance

The disability-related travel-cost lump-sum allowance is to be governed by a new § 33 Abs. 2a EStG. These are therefore extraordinary burdens which, like medical costs and other extraordinary burdens, only have a tax effect if the reasonable personal contribution (zumutbare Belastung) is exceeded. Only the portion exceeding the reasonable personal contribution is deductible.

The lump-sum allowance is intended for:

- Persons with walking and standing impairments with a degree of disability of at least 80, or of at least 70 combined with the identifier "G", in the amount of EUR 900

- Persons with exceptional walking impairments bearing the identifier "aG", blind persons or persons with disabilities bearing the identifier "H", in the amount of EUR 4,500.

Beyond the travel-cost lump-sum allowance, no further disability-related travel costs may be considered as extraordinary burdens.

Waiver of the additional eligibility requirements

To date, the lump-sum allowance is granted to taxpayers with a degree of disability of less than 50 only if

- the disability has led to a permanent impairment of physical mobility,

- the disability is based on a typical occupational illness, or

- the taxpayer is entitled to a statutory pension or benefit due to the disability.

These additional requirements in § 33b Abs. 2 EStG are to be removed without replacement from the 2021 assessment period.

New in the government draft are the planned changes to the care lump-sum allowance (Pflege-Pauschbetrag, § 33b Abs. 6 EStG).

The care lump-sum allowance is also to be claimable irrespective of whether the cared-for person meets the "helpless" criterion.

The care lump-sum allowance for the care of persons with care levels 4 and 5 is to be increased from EUR 924 to EUR 1,800, and a care lump-sum allowance for the care of persons with care levels 2 (EUR 600) and 3 (EUR 1,100) is to be newly introduced.

A prerequisite for granting the care lump-sum allowance is, in addition to home-based care, that the caring taxpayer does not receive any income for providing the care.

Frequently asked questions

Frequently asked questions

What are the lump-sum allowances for persons with disabilities from 2021?

The lump-sum allowances for persons with disabilities under § 33b Abs. 3 EStG are doubled from 2021 onwards. For persons classified as helpless within the meaning of § 33b Abs. 6 EStG and for the blind, the allowance increases from EUR 3,700 to EUR 7,400. The remaining allowances, graduated according to the degree of disability, are also doubled accordingly.

From what degree of disability is the lump-sum allowance granted from 2021 onwards?

The system is being aligned with social security law: a disability will now be recognized starting at a degree of disability of 20 (previously 25). The scale is graduated in 10-point increments up to a degree of disability of 100. In addition, from the 2021 assessment period onwards, the additional eligibility requirements for taxpayers with a degree of disability below 50 no longer apply.

How does the new flat-rate allowance for disability-related travel expenses work?

The new § 33 Abs. 2a EStG introduces a flat-rate allowance for travel expenses. Individuals with walking and standing disabilities with a degree of disability (GdB) of at least 80, or at least 70 with the mark "G," receive EUR 900; those with severe walking disabilities (mark "aG"), blind persons, and individuals with the mark "H" receive EUR 4,500. The flat-rate allowance only has a tax effect as an extraordinary expense to the extent it exceeds the reasonable personal contribution. Additional disability-related travel expenses cannot be deducted alongside it.

What is the care lump-sum allowance by care level from 2021?

The care lump-sum allowance under § 33b Abs. 6 EStG is restructured: EUR 600 for care level 2, EUR 1,100 for care level 3, and EUR 1,800 (up from EUR 924) for care levels 4 or 5. In addition, the criterion 'helpless' for the person being cared for is no longer required.

What are the requirements for the care lump-sum allowance (Pflege-Pauschbetrag)?

The requirement is that the taxpayer provides home-based care for the affected person. In addition, the caregiver must not receive any income for their care services. The former requirement that the person being cared for must be classified as helpless no longer applies.